The ironic thing about people who think they can’t afford to buy a home for themselves, end up buying the home for their landlord. There are several facts that support this notion.

Mortgages, whether held by an owner-occupant or an investor, are usually amortized so that each payment reduces the principal amount owed so that the loan will be repaid totally over the term. A tenant is inadvertently retiring the landlord’s mortgage with his monthly rent.

In most cases, the mortgage payment including taxes and insurance will be lower than the rent tenants are paying. Some experts are saying that we may never again experience the incredibly low mortgage interest rates currently available.

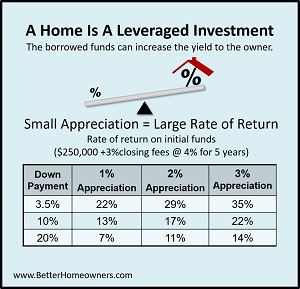

Renting precludes a person from enjoying the advantage a home has as a leveraged investment. When the borrowed funds cost less than the investment is returning, the rate of return on the down payment grows much faster. As you can see from the chart, a 2% appreciation on a home could result in big returns on the down payment. In most cases, there are very few or no alternative investments that offer homeowners similar returns.

Even if a buyer agrees with all of these things but doesn’t have the down payment or cannot qualify for a loan, they still need to investigate further. To find out exactly what types of loans are available and the specific down payment required which can be a whole lot less than 20%, they need to consult with an experienced, trusted loan professional (an Internet lender or a “BIG” bank may not be the best choice.) Call for a recommendation.

---------------------------------------------------------------------------------

If you are serious about making Home Ownership a reality, contact me to schedule your Homebuying Consultation. During this meeting we discuss your "must haves", "wishes" & "deal breakers". I also provide an overview of the Home Buying Process. What you should expect, what happens when the unexpected happens, and much more. Most importantly, we discuss your expectations of me and vice versa, and I answer all of their questions.

If Homebuying is a goal, but you're not sure how or where to begin, let's start with a Get-Homebuying Ready Consultation. At the end of our meeting, you will know what your buying ability is currently and what actions you need to take / things you need to work on to achieve your goal of home ownership. We'll put a plan in place and you'll feel confident about moving forward!

I look forward to assisting you! -Natasha (404) 857-2508